Blockchain technology is like the internet in that it has a build-in robutness. By storing block of information that are identical across its network, the blockchain cannot:

1. Be controlled by any single entity.

2. Has no single point of failure.

1. Be controlled by any single entity.

2. Has no single point of failure.

Bitcoin was invented in 2008. Since that time, the Bitcoin blockchain has operated without significant disruption. (To date, any of problems associated with Bitcoin have been due to hacking or mismanagement. In other words, these problems come from bad intention and human error, not flaws in the underlying concepts.)

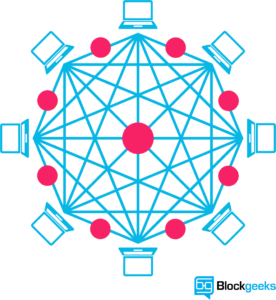

A network of nodes

A network of so-called computing “nodes” make up the blockchain.

Node

(computer connected to the blockchain network using a client that performs the task of validating and relaying transactions) gets a copy of the blockchain, which gets downloaded automatically upon joining the blockchain network.

Together they create a powerful second-level network, a wholly different vision for how the internet can function.

Every node is an “administrator” of the blockchain, and joins the network voluntarily (in this sense, the network is decentralized). However, each one has an incentive for participating in the network: the chance of winning Bitcoins.

Nodes are said to be “mining” Bitcoin, but the term is something of a misnomer. In fact, each one is competing to win Bitcoins by solving computational puzzles. Bitcoin was the raison d’etre of the blockchain as it was originally conceived. It’s now recognized to be only the first of many potential applications of the technology.

There are an estimated 700 Bitcoin-like cryptocurrencies (exchangeable value tokens) already available. As well, a range of other potential adaptations of the original blockchain concept are currently active, or in development.

Beside Bitcoin, Ethereum, the second popular cryptocurrency and blockchain system, is based on the use of token which can be bought, sold, or traded. There are several different tokens which may be used in conjunction with Ethereum, and these differ from ether, which is the currency native to the Ethereum blockchain. Tokens, in the case, represent digital assets that can have variety of values attached. They can represent assets as diverse as vouchers, IOUs, or event object in the real world. In this way, tokens are essentially smart contracts that make use of the Ethereum blockchain. One of the most significant token standards of all for Ethereum is called ERC-20, whcih was developed about year and a half-ago.

Beside Bitcoin, Ethereum, the second popular cryptocurrency and blockchain system, is based on the use of token which can be bought, sold, or traded. There are several different tokens which may be used in conjunction with Ethereum, and these differ from ether, which is the currency native to the Ethereum blockchain. Tokens, in the case, represent digital assets that can have variety of values attached. They can represent assets as diverse as vouchers, IOUs, or event object in the real world. In this way, tokens are essentially smart contracts that make use of the Ethereum blockchain. One of the most significant token standards of all for Ethereum is called ERC-20, whcih was developed about year and a half-ago.

ERC-20 Empowers Developers

In short, the ERC-20 defines a common list of rules all Ethereum tokens to follow, meaning that this particular token empowers developers of all types to accurately predict how new tokens will function within the larger Ethereum system. The impact that ERC-20 therefore has on developers is massive, as projects do not need to be redone each time a new token is released. Rather, they are designed to be compatible with new tokens, provided those tokens adhere to the rules. Developers of new tokens have by-and large observed the ERC-20 rules, meaning that most of the tokens released through Ethereum initial coin offerings are ERC-20 compliant.

No comments:

Post a Comment